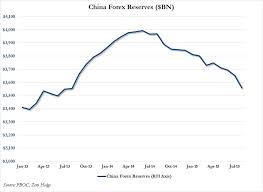

Shortly after the PBoC’s move to devalue the yuan, we noted with some alarm that it looked as though China may have drawn down its reserves by more than $100 billion in the space of just two weeks. That, we went on the point out, would represent a stunning increase over the previous pace of the country’s reserve draw down, which we began documenting months ahead of the devaluation (see here, for instance). We went on to estimate, based on the projected size of the RMB carry trade unwind, how large the FX reserve liquidation might need to be to offset capital outflows and finally, late last week, we suggested that China’s official FX reserve data was set to become the new risk-on/off trigger for nervous, erratic markets. In short, the pace at which Beijing is burning through its USD assets in defense of the yuan has serious implications not only for investors’ collective perception of market stability, but for yields on core paper, for global liquidity, and for US monetary policy.

On Monday we got the official data from China and sure enough, we find out that the PBoC liquidated around $94 billion in reserves during the month of August to $3.557 trillion (the lowest since September 2013)…